I was not happy with my article Carrier Billing and Micropayments, when I first published it over a year ago. I did not feel that the ideas I was trying to communicate were distilled into a coherent formulation. What follows here is a second attempt at trying to convince Communications Service Providers (CSPs) to stop selling dumb pipes.

Most CSPs are old incumbent carriers with large loyal customer bases, established business models, and products that are substantially unchanged for decades. These enterprises are risk-averse. There is little tolerance for changes that would be disruptive to how business is run.

CSPs are in the business of selling dumb pipes (e.g., Internet access, mobile phones). The dumb pipe business is experiencing decreasing revenue per bit. CSPs know that this trend of diminishing profitability is unhealthy, and they are highly motivated to expand into new products (e.g., video).

Since the rise of the Internet, CSPs have seen Over The Top (OTT) services (Internet platformed services) thrive. OTT providers have even invaded the CSP’s spaces. While CSPs expanded into television and video services, OTT video services like Netflix and Hulu caused many customers to terminate their traditional television services. Customers prefer unbundled video streaming. This is especially true now that Disney Plus, ESPN+, HBO Max, and other premium video packages have become available à la carte (no longer exclusively bundled with television service). Unbundling of video services is once again relegating CSPs to selling dumb pipes, which undermines their efforts to expand revenues up the value chain.

CSPs have stodgy business models, because they are afraid of competition further eating into their revenue. CSPs suffer from their inability to formulate new product strategies to better monetize 5G investments. Technical features like network slicing, low latency, higher reliability, low power, high bandwidth, expanded radio spectrum offer possibilities for innovative applications, but carriers have struggled to translate such potential into desirable products beyond the standard offerings for the already saturated market for mobile phone service with mobile data.

From Tom Nolle:

- Will 5G Really Open New Revenue Opportunities? – December 18, 2018

- 5G Pricing, Progress, and Missions – August 20, 2020

- How Telcos Can Still Save Themselves – March 29, 2021

- A Planners’ Perspective on 5G – December 1, 2022

- Why are Operators Forecasting a Capex Crunch, and What Could be Done? – January 12, 2023

Other articles:

- How will 5G unlock revenue streams and increase profitability? – October 14, 2019

- Study: Telco industry struggles to find new profits in 5G technology – January 16, 2020

- 5G and the new revenue opportunities available to CSPs – September 7. 2021

Beyond 5G mobile and fixed wireless features, CSPs also have ambitions of expanding revenues through Edge Computing and “carrier cloud”. CSPs view the construction of their own cloud infrastructure in their own data centers as a core competency that is strategically important to the operation of the Network Functions that provide their communications services over their own network infrastructure.

Again, from Tom Nolle:

- The Evolution of the Carrier Cloud – February 7, 2017

- Carrier Cloud and Edge Computing Connections – June 17, 2019

- How Operator Planners View Carrier Cloud – April 30, 2020

CSPs have ambitions to offer products to their customers based on carrier cloud, but they suffer from competition from hyperscalers (AWS, Microsoft Azure, Google Cloud Platform, Oracle, IBM). They aim to leverage their own data centers to provide cloud services for Edge Computing at the provider edge, believing that low latency in the last mile to the customer will offer performance advantages to certain types of services. Unfortunately, there is no evidence that such an advantage exists for CSPs. Performance sensitive components would likely need to be deployed at the customer edge in close proximity to the customer’s devices (such as for near real-time control of industrial processes). For all other types of services, it is difficult to see how regional CSPs can compete on price, scale, and reach against hyperscalers, who have global reach and performance characteristics that are not materially disadvantageous for those use cases. If customers need the performance, they will need computing at the customer edge. Otherwise, when their requirements are less stringent, public cloud infrastructure from hyperscalers is sufficient and economically advantageous.

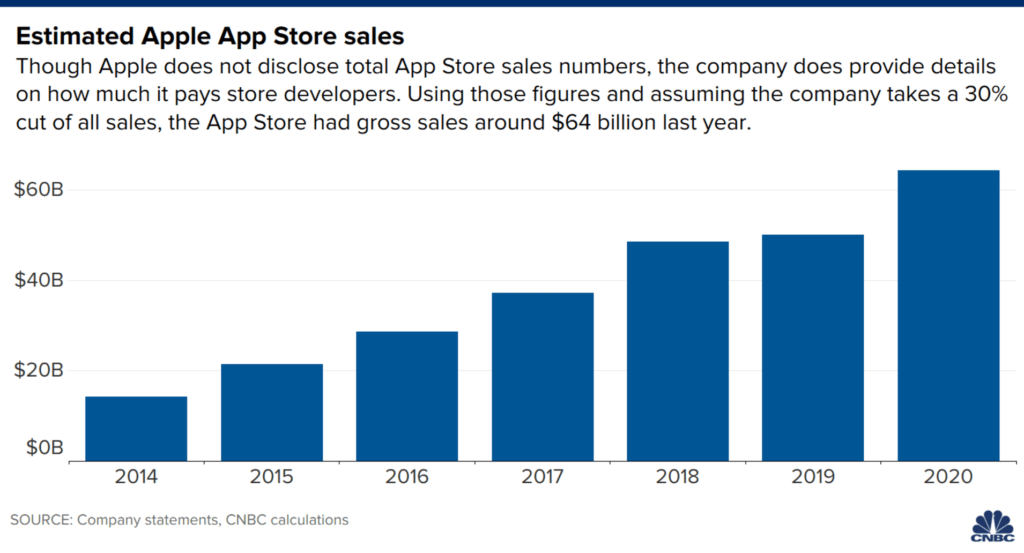

CSPs must become more open to transforming their business models to find better revenue opportunities. They should look to Apple’s market success as one example of how to think differently. Apple forged a lucrative business model based on their iPhone and iOS ecosystem by taking a 30% cut of third party revenues earned by distributing applications through the Apple App Store. Because the potential for applications and in-app purchases is unbounded, the opportunities are enormous for Apple to earn revenues based on the innovations and work of innumerable third-parties using Apple’s platform. This is proven out by Apple’s incredible financial performance since launching this ecosystem.

CSPs should look to where their own businesses have strengths and advantages. CSPs have a large and established customer base, who entrusts the carrier to take automatic payments every month. That kind of trust relationship and reliable revenue stream is precious. Carriers have not learned to monetize that relationship with OTT service partners or extend such relationships to third parties, as Apple does. One of the biggest impediments to online businesses converting sales for digital subscriptions is the resistance among customers to trust the business enough to create an account and authorize their payment card for automatic recurring payments. That lack of trust is an enormous barrier for most businesses. CSPs can leverage their advantage in Carrier billing to enable micropayments and easier monetization of third party services through the carrier’s infrastructure, billing, and payment platforms. This would enable CSPs to apply Apple’s business model to charge third party services a percentage of subscription fees by owning the customer relationship and the monetization of those third party services.

Let’s explore a concrete scenario to illustrate this point. As a customer of online digital services, each of us has routinely been the victim of multiple unscrupulous vendors. One crooked technique these vendors employ is to be unresponsive to termination requests for subscriptions that have recurring monthly payments automatically charged to a payment card. Sometimes such paid subscriptions are opted in by misleading a customer to try a free introductory offer. Often, intervention from the bank or payment card company is required as a remedy. These kinds of costly and upsetting incidents ruin it for all online digital services, because customers become wary of authorizing payments for any business whose reputation is unknown. Every time a customer shares their payment card information with another vendor, it is a calculated risk that the vendor could be unscrupulous or that the payment card information can be stolen by a data breach (hacking). After being burned, most people would be extremely hesitant to subscribe to a dozen low cost ($0.99 per month) content providers (i.e., magazines, journals, newspapers, etc.), each taking payments separately.

However, for a customer already being charged $200 per month by a CSP for their family’s multiple mobile phone and data services, adding an extra twelve $0.99 charges to their bill (an increase of less than 6%) with the peace of mind knowing that the carrier’s billing dispute and adjustment processes are reputable, friendly, and reliable is a comfortable commitment to enroll in. Now, imagine every product company taking advantage of this easy entry into the market for digital subscriptions, where they would otherwise have found the barrier to entry too daunting. You will see connected running shoes, connected tennis rackets, connected exercise equipment, connected vehicle dash cameras, connected home security cameras, connected home appliances, connected irrigation systems, connected pool circulation systems, connected everything become viable market opportunities for the smallest (and most innovative and entrepreneurial) of vendors. If CSPs bundled monetization with access to their 5G capabilities and their Edge Computing resources for a cut of the third party service’s revenues, that arrangement becomes even more attractive to innovative and entrepreneurial startups who may build the next killer app that no CSP could dream of themselves—and that would be impossible to nurture into existence through partnerships.

For CSPs who envision that the Internet of Things (IoT) will provide new revenue streams in high volumes, they must realize that for things to be connected to the Internet in an economical way, the digital services associated with those things must be monetizable easily and with low barrier to entry. For there to be sufficient uptake, not only do ordinary physical things in everyone’s every day lives need to be connected, but it must be inexpensive and convenient. Technical capabilities, convenience, and low cost come about by leveraging the CSP’s infrastructure, services, monetization platform, and established relationship with the customer base.

As a stodgy incumbent, a CSP is resistant to revamping how they do business. Their belief in their products is entrenched. They believe their own role in the market is entrenched. Incumbency and entrenchment are impediments to transforming their business. So long as CSPs cling to the belief that they must defend their declining revenue-per-bit dumb pipe business against OTT services, CSPs will not be motivated to engage in transformation. They need to understand that their advantage is not in dumb pipes. Their advantage is in owning strong customer relationships that can be monetized on behalf of third party services that are unbounded in potential revenue opportunities. Digital services want to receive payments from subscribers, and CSPs can broker this through their own reputable, ethical, and trust-worthy billing and payments platform.

CSPs must move away from primarily selling dumb pipes. They should re-orient the business to enable an ecosystem that uses the CSP’s infrastructure and platform to sell digital services from all vendors to the installed base of loyal customers. This will open up unbounded opportunities for passive income as all the risk to develop innovative new products based on OTT services is borne by third party digital service providers, while the CSP reaps the rewards of their use of the CSP’s ecosystem.

«Asian operators have moved on from 5G

. . .

Asian operators have moved on to new services. SKT is turning itself into an AI company. KT Corp is growing its media and cloud business. In neighboring Japan, just emerging from a 5G price war, telcos are leaning into a broad swathe of growth drivers such as financial and smart services.»

https://www.lightreading.com/5g-and-beyond/asian-operators-have-moved-on-from-5g/d/d-id/784967

«telecom indeed has three years maximum to come up with a different business model»

https://andoverintel.com/2023/09/27/did-the-dwt23-conference-provide-insights-into-telcos-service-future/